FHA Seller Concession Guidelines

Understanding FHA seller concession guidelines helps homebuyers reduce out-of-pocket expenses during the purchase process. Sellers can contribute funds toward buyer closing costs, making homeownership more accessible for qualified borrowers. These contributions are subject to specific limits established by the Federal Housing Administration to protect both parties in real estate transactions.

Understanding FHA seller concession guidelines helps homebuyers reduce out-of-pocket expenses during the purchase process. Sellers can contribute funds toward buyer closing costs, making homeownership more accessible for qualified borrowers. These contributions are subject to specific limits established by the Federal Housing Administration to protect both parties in real estate transactions.

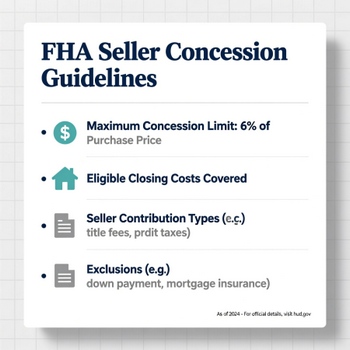

The FHA max seller concessions allow sellers to pay up to 6% of the home's purchase price or appraised value toward buyer expenses. This limit exceeds many conventional loan programs and provides financial relief for buyers with limited cash reserves. Loan requirements specify exactly how these funds can be used during closing.

Buyers who understand these guidelines gain negotiating advantages in competitive real estate markets. Sellers benefit from making their properties more attractive to potential buyers through financial assistance. Real estate professionals often structure deals using FHA seller concessions to facilitate successful transactions.

What Are FHA Seller Concessions and How They Work

FHA allowable seller concessions represent financial contributions sellers make toward buyer expenses during the mortgage process. These concessions cover various closing costs, prepaid items, and fees associated with obtaining financing. The lending industry recognizes these payments as legitimate components of transactions that benefit both buyers and sellers.

Mortgage lenders review concessions during underwriting to verify compliance with program guidelines. The contribution amount cannot exceed actual closing costs and prepaid expenses, regardless of the percentage limit. Any excess concessions must be applied toward principal reduction or returned to the seller at closing.

FHA loans and closing costs work together to determine how much financial assistance buyers need. Sellers can pay origination fees, title insurance, appraisal costs, and prepaid property taxes within the established limits. These contributions significantly reduce the cash buyers must bring to closing.

FHA Max Seller Credit Limits and Contribution Rules

The FHA seller credit limit stands at 6% of the lesser amount between purchase price and appraised value. This cap applies to all FHA-insured mortgages regardless of property type or location. Conventional loans typically allow only 3% to 9% down payment, depending on the loan purpose and the down payment amount.

FHA interested party contributions include payments from sellers, real estate agents, builders, or other parties with financial interest in the transaction. All contributions from interested parties combined cannot exceed the 6% threshold. This rule prevents excessive concessions that might artificially inflate purchase prices.

Buyers making the minimum 3.5% down payment can still receive max seller concessions FHA 3.5 down offers up to the full 6% limit. The down payment requirement and concession limits operate independently under FHA guidelines. Down payment calculations help buyers understand their total cash requirements.

Allowable Expenses Covered by Seller Contributions

FHA maximum seller concessions can cover many buyer expenses during the closing process. Understanding which costs qualify helps buyers and sellers structure effective agreements. The following expenses typically qualify for seller contribution coverage:

- Loan origination fees and discount points charged by lenders

- Title insurance premiums, escrow fees, and settlement charges

- Property appraisal costs and credit report expenses

- Prepaid homeowners insurance and property tax reserves

- Home inspection fees and property survey costs

- Recording fees and transfer tax amounts

FHA seller contribution limits specifically exclude certain expenses from concession coverage. Down payment funds cannot come from seller concessions under any circumstances. Cash reserve requirements, personal property purchases, and some third-party fees also fall outside allowable concession uses.

Interest rate buydowns are a popular use of seller concessions, in which sellers pay fees to reduce buyers' mortgage rates. Temporary buydowns lower payments during the initial loan years, while permanent buydowns reduce rates for the entire loan term. Buydown calculators show potential monthly payment savings from these strategies.

FHA Concession Limits vs Other Loan Programs

FHA concession limits provide more flexibility than many conventional mortgage programs. Conventional loans typically cap seller concessions at 3% to 9%, depending on the down payment amount and occupancy type. Investment property purchases are subject to stricter limits under conventional guidelines.

USDA loan programs allow seller concessions up to 6%, similar to FHA requirements for rural property purchases. VA loans permit sellers to pay all buyer closing costs without percentage caps, offering the most generous concession allowances. These differences affect which loan program buyers choose based on their financial situations.

Negotiating Seller Concessions in Different Markets

Market conditions significantly impact seller willingness to offer concessions and buyer ability to negotiate favorable terms. Strong seller markets with limited inventory reduce concession opportunities due to competition among buyers. Multiple offer situations often eliminate concession possibilities entirely.

Buyer markets with abundant housing supply increase FHA IPC limits negotiation success rates. Sellers in these conditions often agree to maximum concession amounts to attract qualified offers. Properties requiring repairs or updates present additional opportunities for concession negotiation.

Inspection requirements sometimes reveal property issues that support concession requests. Buyers can negotiate seller contributions to cover repair costs or closing expenses based on inspection findings. Real estate agents help structure these negotiations effectively.

How Appraisals Affect Seller Concession Amounts

Property appraisals play critical roles in determining actual max seller concessions FHA amounts available. The 6% limit applies to whichever is lower: the purchase price or the appraised value. Low appraisals reduce maximum concession dollars even when percentages remain constant.

Buyers and sellers must adjust agreements when appraisals come in below purchase prices. The reduced property value lowers both the loan amount and maximum allowable concessions. This situation sometimes requires buyers to bring additional cash or renegotiate purchase terms. Loan-to-value calculations help determine how appraisal values affect financing amounts. Buyers should understand these relationships before making purchase offers. Professional appraisals protect all parties by establishing accurate property values for lending purposes.

Documentation Requirements for Seller Concessions

Proper documentation ensures FHA allowable seller concessions comply with program guidelines during underwriting review. Purchase agreements must clearly state concession amounts and intended uses. Settlement statements show exact expense allocations at closing. Lenders require detailed breakdowns of how seller contributions apply to specific closing costs. Vague concession language in purchase contracts creates underwriting delays and potential approval issues. Underwriting processes verify all concession documentation meets FHA standards. Real estate agents and closing attorneys ensure proper concession documentation throughout transactions. These professionals understand regulatory requirements and prepare necessary paperwork correctly. Accurate documentation prevents last-minute complications that could jeopardize closing dates.

Strategic Planning for Maximum Concession Benefits

Effective concession planning begins during pre-approval conversations with mortgage lenders. Buyers should discuss potential concession needs based on estimated closing costs and available cash reserves. Affordability calculators help buyers understand total purchase costs including concessions.

Timing significantly affects concession negotiations throughout the purchase process. Early concession discussions enable parties to structure offers effectively from the start. Last-minute concession requests create complications that may delay closings or reduce negotiating leverage.

Professional guidance from experienced real estate agents and mortgage professionals maximizes concession benefits while maintaining loan eligibility. These experts thoroughly understand current market conditions and program requirements. Getting an FHA loan involves coordinating multiple transaction components successfully.

Common Concession Mistakes to Avoid

Buyers sometimes request concessions exceeding actual closing costs, creating underwriting issues when excess funds have nowhere to go. Accurate cost estimates prevent this problem. Lenders cannot approve concessions that exceed legitimate expenses regardless of the 6% limit.

Inflated purchase prices to accommodate higher concession amounts raise red flags during underwriting review. Appraisers identify these situations through comparable sales analysis. Avoiding common FHA mistakes improves approval chances significantly.

Mixing gift funds with seller concessions sometimes creates confusion about down payment source requirements. Gift fund guidelines differ from concession rules and require separate documentation. Buyers must understand these distinctions to structure transactions properly.

Future Trends in Seller Concession Guidelines

FHA periodically reviews concession limits and may adjust guidelines based on housing market conditions and economic factors. Current FHA requirements reflect the most recent program updates. Buyers and sellers should stay informed about potential changes to guidelines.

Interest rate environments influence how buyers use seller concessions strategically. Higher rates increase demand for rate buydown concessions while lower rates shift focus toward closing cost coverage. Monitoring interest rates helps buyers make informed concession decisions.

Economic conditions and housing supply levels continue affecting concession negotiation dynamics. Understanding these broader trends enables buyers and sellers to develop effective strategies. Professional guidance remains valuable for successfully navigating evolving market conditions.

Frequently Asked Questions About FHA Seller Concessions

Can seller concessions cover my entire down payment on an FHA loan?

No, seller concessions cannot cover any portion of the required down payment under FHA guidelines. Buyers must provide the minimum 3.5% down payment from their own funds or eligible gift sources. Seller concessions apply only to closing costs and prepaid expenses, not to down payment amounts.

What happens if seller concessions exceed my actual closing costs?

When seller concessions exceed actual closing costs, the excess amount must either be applied toward principal reduction on the mortgage or returned to the seller at closing. Lenders cannot approve concessions that exceed legitimate buyer expenses regardless of the 6% limit.

Do seller concessions affect my interest rate or loan approval?

Seller concessions themselves do not directly affect interest rates or loan approval decisions. However, buyers can use concessions to purchase discount points that lower interest rates. Lenders evaluate concessions during underwriting to ensure compliance with FHA guidelines and to prevent artificially inflated purchase prices.

Can I negotiate seller concessions after my offer is accepted?

While possible, negotiating concessions after offer acceptance is more difficult than including them in the initial purchase agreement. Inspection findings or appraisal issues sometimes justify concession requests during the transaction. However, sellers have less incentive to agree once contracts are signed.

Are FHA seller concession limits the same for refinance transactions?

FHA refinance transactions have different rules than purchase loans regarding seller contributions. Rate and term refinances generally prohibit seller concessions entirely. Cash-out refinances may allow limited concessions on specific closing costs, but such concessions are less common than those in purchase transactions.

Connect With Us

Please share – it really helps